Ahmedabad

(Head Office)Address : 506, 3rd EYE THREE (III), Opp. Induben Khakhrawala, Girish Cold Drink Cross Road, CG Road, Navrangpura, Ahmedabad, 380009.

Mobile : 8469231587 / 9586028957

E-mail: dics.upsc@gmail.com

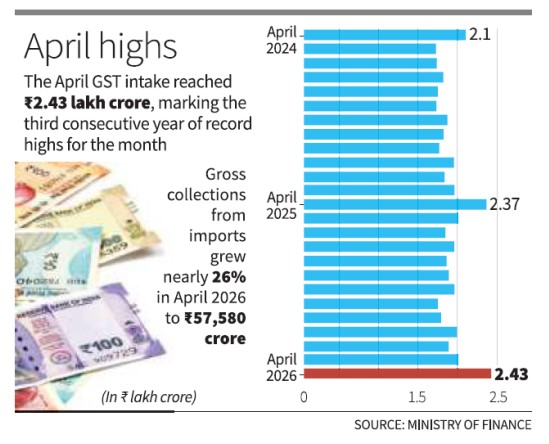

• Historic Achievement: India’s Gross Goods and Services Tax (GST) revenue reached an unprecedented peak of ₹2.43 lakh crore in April 2026, marking an 8.7% year-on-year growth compared to the same month in 2025.

• Net Revenue Position: After accounting for tax refunds, the net GST collection stood at ₹2.11 lakh crore, reflecting a 7.3% increase, which indicates a robust underlying tax base despite global economic volatility.

• Import-Led Growth: The primary catalyst for this record surge was revenue from imports, which grew by nearly 26% to ₹57,580 crore, while domestic transaction growth remained relatively modest at 4.3% (₹1.85 lakh crore).

• The March Effect: Tax experts attribute the annual April spike to the financial year-end push, where businesses and tax administrators finalize accounts for March to meet annual fiscal targets, a trend consistent since the 2017 rollout (excluding the 2020 pandemic year).

• Resilience Amid Headwinds: This fiscal performance is significant as it occurred despite geopolitical tensions in West Asia and broader global economic uncertainty, signaling strong domestic consumption and effective tax administration.

• Composition of Collections: The gross figure comprises Central GST (CGST), State GST (SGST), Integrated GST (IGST) on both domestic and imported goods, and the Compensation Cess levied on demerit goods.

Key Definitions & Concepts

• IGST (Integrated GST): Levied on all Inter-State supplies of goods and/or services and also on imports. It is collected by the Centre and then apportioned between the Union and the States.

• Net GST Revenue: The gross amount collected minus the refunds issued to taxpayers (such as exporters or those with an inverted duty structure).

• Inverted Duty Structure: A situation where the tax rate on inputs purchased is higher than the tax rate on finished goods sold, leading to a buildup of input tax credit.

Constitutional & Legal Provisions

• 101st Constitutional Amendment Act, 2016: Introduced the GST regime in India, fundamentally altering the fiscal federalism landscape by subsuming various Central and State indirect taxes.

• Article 246A: Grants Parliament and State Legislatures concurrent power to make laws with respect to GST. However, Parliament has exclusive power to legislate on GST where the supply takes place in the course of inter-state trade.

• Article 279A: Provides for the constitution of the GST Council, a joint forum of the Centre and States, chaired by the Union Finance Minister, to make recommendations on tax rates, exemptions, and thresholds.

• GST Compensation Cess: Originally intended to compensate states for revenue loss for five years, it continues to be levied to repay loans taken during the pandemic period.

Additional Key Points for Analysis

• Compliance & Tech Integration: Increased collections are also linked to the strengthening of the GSTN (GST Network) and the use of deep data analytics to curb tax evasion and fake invoicing.

• Consumption Patterns: The slower growth in domestic collections (4.3%) compared to imports (26%) may prompt policy discussions regarding the cooling of domestic demand versus the buoyancy of the external trade sector.

Conclusion

The record-breaking collection of ₹2.43 lakh crore underscores the maturity and stability of the GST regime as it enters its ninth year. While the April peak is seasonally anticipated, the consistent upward trajectory validates the formalization of the Indian economy. Moving forward, the focus will likely shift toward rationalizing the multiple tax slabs and addressing the widening gap between domestic and import-led revenue growth to ensure sustainable fiscal health.

UPSC Relevance

• General Studies II: Issues relating to federal structure (GST Council), Statutory/Regulatory bodies, and Constitutional amendments.

• General Studies III: Indian Economy and issues relating to planning, mobilization of resources, growth, and development. Fiscal Policy and Government Budgeting.

Address : 506, 3rd EYE THREE (III), Opp. Induben Khakhrawala, Girish Cold Drink Cross Road, CG Road, Navrangpura, Ahmedabad, 380009.

Mobile : 8469231587 / 9586028957

E-mail: dics.upsc@gmail.com

Address: A-306, The Landmark, Urjanagar-1, Opp. Spicy Street, Kudasan – Por Road, Kudasan, Gandhinagar – 382421

Mobile : 9723832444 / 9723932444

E-mail: dics.gnagar@gmail.com

Address: 2nd Floor, 9 Shivali Society, L&T Circle, opp. Ratri Bazar, Karelibaugh, Vadodara, 390018

Mobile : 9725692037 / 9725692054

E-mail: dics.vadodara@gmail.com

Address: 403, Raj Victoria, Opp. Pal Walkway, Near Galaxy Circle, Pal, Surat-394510

Mobile : 8401031583 / 8401031587

E-mail: dics.surat@gmail.com

Address: 303,305 K 158 Complex Above Magson, Sindhubhavan Road Ahmedabad-380059

Mobile : 9974751177 / 8469231587

E-mail: dicssbr@gmail.com

Address: 57/17, 2nd Floor, Old Rajinder Nagar Market, Bada Bazaar Marg, Delhi-60

Mobile : 9104830862 / 9104830865

E-mail: dics.newdelhi@gmail.com