Ahmedabad

(Head Office)Address : 506, 3rd EYE THREE (III), Opp. Induben Khakhrawala, Girish Cold Drink Cross Road, CG Road, Navrangpura, Ahmedabad, 380009.

Mobile : 8469231587 / 9586028957

Telephone : 079-40098991

E-mail: dics.upsc@gmail.com

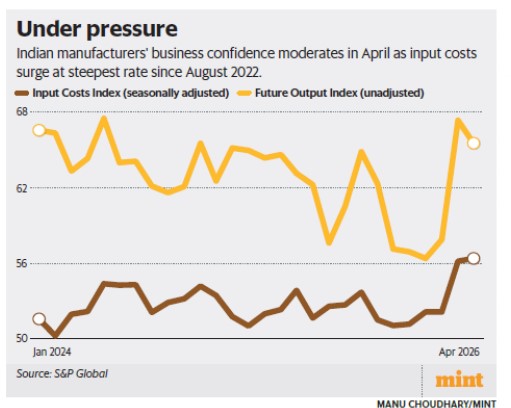

• Marginal Upswing in Momentum: The HSBC India Manufacturing Purchasing Managers Index (PMI) rose to 54.7 in April from 53.9 in March; however, this remains the second-slowest improvement in operating conditions in nearly four years, suggesting a lukewarm recovery.

• Input Cost Inflation: Manufacturers are facing the sharpest rise in input costs since August 2022, driven primarily by soaring crude oil prices and supply-chain disruptions linked to the US-Iran conflict, leading to significant imported inflation.

• Inventory Front-Loading: The slight uptick in April is attributed to pre-emptive buying where consumers purchased goods before anticipated retail price hikes, and manufacturers built up inventories before energy costs escalated further.

• Currency and Logistics Pressures: The Indian Rupee breaching the 95/$ mark has made imported raw materials substantially dearer, while the potential post-election hike in retail fuel prices threatens to increase logistics costs and dampen consumer purchasing power.

• Export Resilience vs. Future Confidence: While new export orders reached a seven-month high due to demand from markets like the UAE, UK, and China, the overall business confidence sub-index for future sales has dipped, reflecting uncertainty about sustained domestic demand.

• Margin Protection vs. Volume Growth: To protect profit margins from rising WPI (which hit 3.88% in March), goods producers have raised selling prices at the fastest rate in six months, a move that risks slowing down sales volumes if inflation persists.

Key Definitions

• Purchasing Managers Index (PMI): An economic indicator derived from monthly surveys of private sector companies. A reading above 50 signals expansion, while below 50 indicates contraction.

• Wholesale Price Index (WPI): An index that measures and tracks the changes in the price of goods in the stages before the retail level (bulk prices).

• Imported Inflation: A rise in domestic prices caused by an increase in the costs of imported raw materials or finished goods, often exacerbated by currency depreciation.

Constitutional & Legal Provisions

• Article 246 (Seventh Schedule): Taxes on the sale or purchase of goods (GST) fall under the concurrent legislative power, influencing the final pricing and PMI sentiment.

• Article 292: Relates to the executive power of the Union to borrow upon the security of the Consolidated Fund of India, which is impacted by fiscal pressures arising from high oil prices and subsidies.

• RBI Act, 1934: Mandates the Reserve Bank of India to maintain price stability while keeping in mind the objective of growth, directly linking PMI data to future repo rate decisions.

Additional Key Points for Examination

• Sectoral Contribution: Manufacturing contributes approximately 17% to India\'s GDP; a stagnation in PMI suggests a potential slowdown in reaching the target of 25% under the National Manufacturing Policy.

• High-Frequency Indicators: Despite PMI concerns, robust bank credit growth (16.1%) and strong GST collections provide a constructive counter-narrative to the manufacturing slowdown.

• The K-Shaped Risk: Rising selling prices may lead to a scenario where affluent demand remains steady while rural and lower-income consumption (more sensitive to fuel/food inflation) contracts.

Conclusion

While the April PMI shows a numerical recovery, the underlying drivers suggest a fragile stabilization rather than a robust expansion. The convergence of currency depreciation, geopolitical energy shocks, and the exhaustion of pre-emptive buying creates a challenging environment for the Make in India initiative. Moving forward, the manufacturing sector health will depend heavily on the stabilization of the Rupee and the government\'s ability to manage the pass-through of energy costs without stifling domestic consumption.

UPSC Relevance

• General Studies III (Economy): Indicators of economic growth, inflation management, and the impact of global supply chains on domestic manufacturing.

• General Studies II (International Relations): Impact of West Asian conflicts on India’s energy security and macroeconomic stability.

• Prelims: Understanding the components of PMI, the difference between WPI and CPI, and the impact of Rupee depreciation on the Trade Balance.

Address : 506, 3rd EYE THREE (III), Opp. Induben Khakhrawala, Girish Cold Drink Cross Road, CG Road, Navrangpura, Ahmedabad, 380009.

Mobile : 8469231587 / 9586028957

Telephone : 079-40098991

E-mail: dics.upsc@gmail.com

Address: A-306, The Landmark, Urjanagar-1, Opp. Spicy Street, Kudasan – Por Road, Kudasan, Gandhinagar – 382421

Mobile : 9723832444 / 9723932444

E-mail: dics.gnagar@gmail.com

Address: 2nd Floor, 9 Shivali Society, L&T Circle, opp. Ratri Bazar, Karelibaugh, Vadodara, 390018

Mobile : 9725692037 / 9725692054

E-mail: dics.vadodara@gmail.com

Address: 403, Raj Victoria, Opp. Pal Walkway, Near Galaxy Circle, Pal, Surat-394510

Mobile : 8401031583 / 8401031587

E-mail: dics.surat@gmail.com

Address: 303,305 K 158 Complex Above Magson, Sindhubhavan Road Ahmedabad-380059

Mobile : 9974751177 / 8469231587

E-mail: dicssbr@gmail.com

Address: 57/17, 2nd Floor, Old Rajinder Nagar Market, Bada Bazaar Marg, Delhi-60

Mobile : 9104830862 / 9104830865

E-mail: dics.newdelhi@gmail.com