Ahmedabad

(Head Office)Address : 506, 3rd EYE THREE (III), Opp. Induben Khakhrawala, Girish Cold Drink Cross Road, CG Road, Navrangpura, Ahmedabad, 380009.

Mobile : 8469231587 / 9586028957

E-mail: dics.upsc@gmail.com

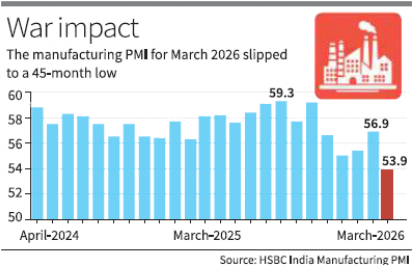

The Indian manufacturing sector faced a significant setback in March 2026, with activity levels dropping to their lowest point in nearly four years. According to the HSBC India Manufacturing Purchasing Managers’ Index (PMI), the escalation of the war in West Asia has triggered a chain reaction of rising input costs, supply chain disruptions, and dampened global demand. While the sector remains in the expansionary zone (above 50), the sharp decline from 56.9 in February to 53.9 in March signals a period of heightened economic uncertainty and cooling industrial momentum. Core Summary of the Economic Slowdown • PMI Slump: The Manufacturing PMI fell to 53.9 in March 2026, marking a 45-month low since June 2022, indicating a substantial loss in growth momentum compared to previous months. • Geopolitical Headwinds: The ongoing war in West Asia (Middle East) is identified as the primary external shock, affecting new order inflows and creating a climate of \'heightened market uncertainty.\' • Steepest Cost Pressures: Input price inflation reached its highest level since August 2022, with firms reporting significant price hikes in essential industrial raw materials like aluminium, steel, chemicals, and fuel. • Slowest Growth in Sub-components: The two most critical drivers of the manufacturing sector—New Orders and Output—grew at their slowest rates in over three and a half years. • Supply Chain Fragility: Increased fuel prices and logistical challenges stemming from the regional conflict have led to an intensification of cost pressures, forcing firms to navigate \'fierce competition\' with squeezed margins. Key Definitions • Purchasing Managers’ Index (PMI): An economic indicator derived from monthly surveys of private sector companies. It acts as a \'lead indicator\' of economic health. A reading above 50 represents expansion, while below 50 indicates contraction. • Input Price Inflation: The rate at which the prices of raw materials and services used in the production process increase. High input inflation often leads to \'Cost-Push Inflation\' in the broader economy. • Anecdotal Evidence: Information based on informal accounts or individual stories from firms (used in PMI reports to explain the \'why\' behind the numbers). Economic & Statutory Context • Index of Industrial Production (IIP): While PMI is a qualitative survey-based indicator, the IIP is the official government quantitative measure of industrial growth (published by NSO). Disparity between the two often provides a deeper look into \'formal vs. informal\' sector health. • Monetary Policy Committee (MPC) Mandate: Under the RBI Act, 1934, the MPC must maintain price stability (target of 4%+/-2%). Rising manufacturing costs due to the West Asia crisis may limit the RBI\'s ability to cut interest rates to spur growth. • Trade Policy & Foreign Trade Act: The slowdown highlights India\'s dependence on stable trade routes in the Persian Gulf and the Red Sea for the import of raw materials and the export of finished goods. Additional Important Keypoints • Commodity Specific Hikes: The report specifically highlights price increases in rubber, leather, jute, and oil, suggesting that the crisis is affecting a wide spectrum of industries from automobiles to textiles. • Employment Outlook: While the PMI covers employment, a slowdown in output and new orders often leads to a \'hiring freeze\' or cautious recruitment strategies by manufacturing firms in the short term. • Export Vulnerability: The conflict in West Asia impacts the \'External Sector\' of the Indian economy, as the region is both a major energy supplier and a key destination for Indian engineering and agricultural exports. Conclusion The March 2026 PMI data serves as a stark reminder of India\'s vulnerability to global geopolitical shocks. The transition from a robust 56.9 to a 53.9 indicates that while the domestic economy has inherent resilience, it cannot remain insulated from the soaring energy costs and logistical bottlenecks caused by the West Asia crisis. For the manufacturing sector to rebound, a combination of diplomatic de-escalation in the Middle East and domestic policy support to mitigate rising input costs will be essential in the coming quarters. UPSC Relevance • GS Paper III (Economy): Highly relevant for topics like \'Changes in Industrial Policy and their effects on industrial growth\' and \'Indian Economy and issues relating to planning, mobilization of resources, and growth.\' • International Relations (GS II): Demonstrates the direct link between \'Regional Conflicts\' and \'Domestic Economic Stability,\' a key theme in India\'s West Asia policy.

Address : 506, 3rd EYE THREE (III), Opp. Induben Khakhrawala, Girish Cold Drink Cross Road, CG Road, Navrangpura, Ahmedabad, 380009.

Mobile : 8469231587 / 9586028957

E-mail: dics.upsc@gmail.com

Address: A-306, The Landmark, Urjanagar-1, Opp. Spicy Street, Kudasan – Por Road, Kudasan, Gandhinagar – 382421

Mobile : 9723832444 / 9723932444

E-mail: dics.gnagar@gmail.com

Address: 2nd Floor, 9 Shivali Society, L&T Circle, opp. Ratri Bazar, Karelibaugh, Vadodara, 390018

Mobile : 9725692037 / 9725692054

E-mail: dics.vadodara@gmail.com

Address: 403, Raj Victoria, Opp. Pal Walkway, Near Galaxy Circle, Pal, Surat-394510

Mobile : 8401031583 / 8401031587

E-mail: dics.surat@gmail.com

Address: 303,305 K 158 Complex Above Magson, Sindhubhavan Road Ahmedabad-380059

Mobile : 9974751177 / 8469231587

E-mail: dicssbr@gmail.com

Address: 57/17, 2nd Floor, Old Rajinder Nagar Market, Bada Bazaar Marg, Delhi-60

Mobile : 9104830862 / 9104830865

E-mail: dics.newdelhi@gmail.com