Ahmedabad

(Head Office)Address : 506, 3rd EYE THREE (III), Opp. Induben Khakhrawala, Girish Cold Drink Cross Road, CG Road, Navrangpura, Ahmedabad, 380009.

Mobile : 8469231587 / 9586028957

Telephone : 079-40098991

E-mail: dics.upsc@gmail.com

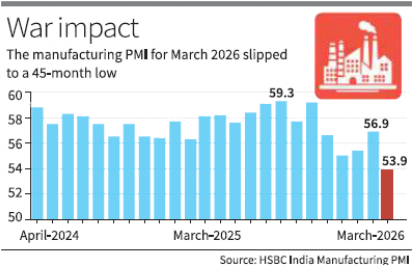

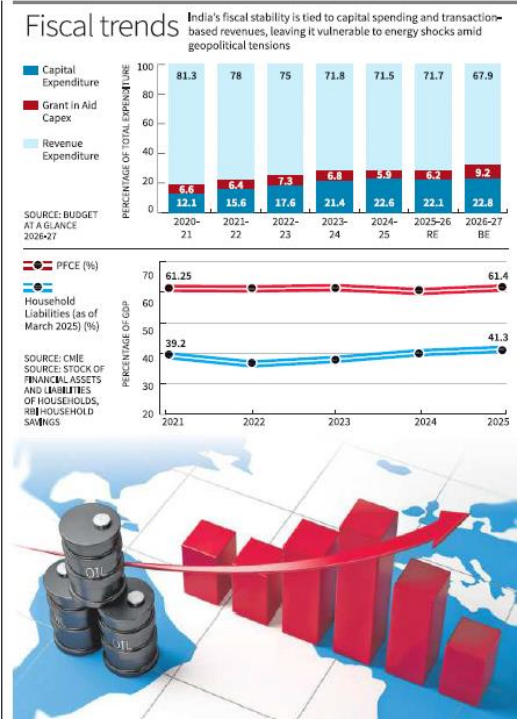

• Macroeconomic Contradiction and External Vulnerability: India currently faces a striking divergence between robust internal indicators and weakening external buffers. While Q3 FY26 GDP growth is projected at 8.1% and public capex remains high (4% of GDP), the Rupee has touched a record low of ₹95 per dollar. Foreign exchange reserves have retreated to $709.76 billion due to FPI outflows of over $8 billion, highlighting that domestic growth prints often mask systemic exposure to global geopolitical shocks. • Energy Import Dependency and Fiscal Squeeze: With India importing 85–87% of its crude oil, the economy remains structurally exposed to price spikes. A $10 per barrel rise in crude typically increases CPI inflation by 0.2 percentage points and reduces GDP growth by 0.5 percentage points. In 2026, with oil hitting $156.29 per barrel, the fiscal space is further compressed as the government must balance excise duty cuts to contain inflation against rising fertilizer and LPG subsidy burdens. • Shift in Revenue Architecture: India’s fiscal model has pivoted toward \'transaction-linked taxation\' (GST) rather than \'income-deepening\' direct taxes. While GST collections reached ₹22.8 lakh crore in FY25, this model is highly sensitive to external shocks. Any disruption in energy markets that slows transport or compresses household spending directly reduces transaction volumes, thereby weakening the primary revenue stream for both the Union and States. • Household Fragility and Leverage: Private consumption, the backbone of the economy (61.4% of GDP), is increasingly sustained by credit rather than real wage growth. Household liabilities have surged to 41% of GDP, making consumers highly vulnerable to \'imported inflation.\' When energy costs rise, real incomes are compressed while fixed debt-servicing obligations remain, creating a \'consumption-debt trap\' that threatens long-term demand stability. • Industrial Divergence and Labor Stress: The industrial recovery is skewed toward capital-intensive, high-tech sectors aligned with public investment, while labor-intensive and informal sectors remain weak. Micro-shocks, such as the 2026 LPG crisis, have caused significant disruptions for small businesses and gig workers, reporting up to a 60% decline in orders. This reflects a lack of institutional protection for the informal economy during geopolitical commodity cycles. Key Definitions and Economic Indicators Indian Basket of Crude Oil: A weighted average of Oman/Dubai (sour) and Brent (sweet) crude price, representing the actual cost of crude for Indian refineries. Fiscal Buoyancy: An indicator of the efficiency of the tax system; it measures the responsiveness of tax revenue growth to changes in GDP. Current Account Deficit (CAD): The shortfall between a nation\'s total export earnings and its total import payments. Capital Expenditure (Capex): Government spending on creating physical assets like roads and power plants, which has a higher \'multiplier effect\' on growth compared to revenue expenditure. Real Wages: Wages adjusted for inflation; they represent the actual purchasing power of a worker\'s income. Conclusion India’s current macroeconomic resilience is being tested by an unprecedented \'energy-geopolitical\' pincer. While the state-led infrastructure push (Capex) builds long-term capacity, the immediate stability of the economy depends on managing the dual pressures of a depreciating currency and imported inflation. Transitioning from a transaction-dependent revenue model to an income-led demand model, alongside aggressive energy diversification, is essential to prevent external shocks from turning into permanent fiscal stress. UPSC Relevance GS Paper III (Indian Economy): Crucial for \'Issues relating to planning, mobilization of resources, growth, development and employment.\' The shift toward GST-linked revenue and rising household debt are vital points for Mains.

Address : 506, 3rd EYE THREE (III), Opp. Induben Khakhrawala, Girish Cold Drink Cross Road, CG Road, Navrangpura, Ahmedabad, 380009.

Mobile : 8469231587 / 9586028957

Telephone : 079-40098991

E-mail: dics.upsc@gmail.com

Address: A-306, The Landmark, Urjanagar-1, Opp. Spicy Street, Kudasan – Por Road, Kudasan, Gandhinagar – 382421

Mobile : 9723832444 / 9723932444

E-mail: dics.gnagar@gmail.com

Address: 2nd Floor, 9 Shivali Society, L&T Circle, opp. Ratri Bazar, Karelibaugh, Vadodara, 390018

Mobile : 9725692037 / 9725692054

E-mail: dics.vadodara@gmail.com

Address: 403, Raj Victoria, Opp. Pal Walkway, Near Galaxy Circle, Pal, Surat-394510

Mobile : 8401031583 / 8401031587

E-mail: dics.surat@gmail.com

Address: 303,305 K 158 Complex Above Magson, Sindhubhavan Road Ahmedabad-380059

Mobile : 9974751177 / 8469231587

E-mail: dicssbr@gmail.com

Address: 57/17, 2nd Floor, Old Rajinder Nagar Market, Bada Bazaar Marg, Delhi-60

Mobile : 9104830862 / 9104830865

E-mail: dics.newdelhi@gmail.com