Ahmedabad

(Head Office)Address : 506, 3rd EYE THREE (III), Opp. Induben Khakhrawala, Girish Cold Drink Cross Road, CG Road, Navrangpura, Ahmedabad, 380009.

Mobile : 8469231587 / 9586028957

Telephone : 079-40098991

E-mail: dics.upsc@gmail.com

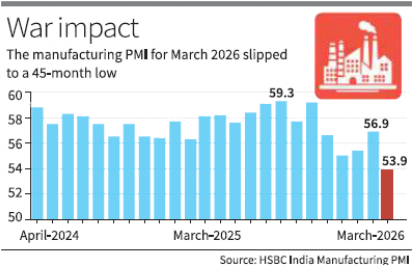

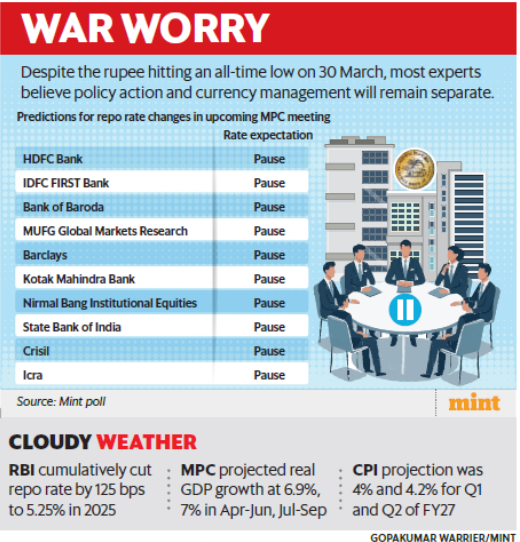

• Expected Rate Pause: The Monetary Policy Committee (MPC) is widely anticipated to maintain the repo rate at 5.25% in its April 2026 meeting. This follows a cumulative 125 bps reduction in 2025, signaling a shift from an accommodative cycle to a \'wait-and-watch\' cautious stance due to geopolitical volatility. • Inflationary Pressures: The West Asia war has triggered a significant surge in Brent crude prices, crossing $100 per barrel. This has led economists to revise Consumer Price Index (CPI) projections upward from 4.1% to approximately 4.7%, driven primarily by \'imported inflation\' and supply chain disruptions. • Downward Growth Revisions: While the RBI previously projected healthy growth, the impact of high energy costs on corporate margins and consumer demand has led private analysts to scale down FY27 GDP estimates from 7% to 6.5%-6.8%. • Currency Volatility: The Indian Rupee has faced depreciation pressure since the conflict began. However, the RBI is expected to manage this through regulatory measures and external interventions rather than using the repo rate as a primary tool to shore up the currency. • Stance Neutrality: The MPC is likely to retain its \'neutral\' stance, providing flexibility to respond to either an inflationary spike or a growth slowdown, while emphasizing that inflation remains within the statutory target band of 4(+/-2)%. • Global Market Disruption: Comparison to the 1973 oil crisis highlights the severity of the current energy market disruption. With oil prices jumping nearly 35% in weeks, the primary challenge for the RBI is balancing the trade-off between price stability and supporting a recovery that is still absorbing the effects of the new GDP series. Key Definitions • Repo Rate: The interest rate at which the Reserve Bank of India lends money to commercial banks against government securities to manage short-term liquidity. • Monetary Policy Committee (MPC): A six-member statutory body under the RBI Act, 1934, responsible for fixing the benchmark interest rate to maintain price stability while keeping the growth objective in mind. • Imported Inflation: A rise in domestic prices caused by an increase in the cost of imported goods, particularly essential commodities like crude oil, which raises production and transport costs across the economy. Constitutional and Legal Provisions • RBI Act, 1934 (Amended 2016): Provides the legal framework for the MPC. Section 45ZB stipulates the constitution of the committee to determine the Policy Rate required to achieve the inflation target. • Inflation Targeting Framework: A statutory requirement where the Central Government, in consultation with the RBI, sets a CPI inflation target every five years. Currently, it is set at 4% with an upper tolerance of 6% and a lower tolerance of 2%. • Article 246: While not directly governing the RBI, the Union List (List I) gives Parliament the exclusive power to legislate on matters related to Currency, Coinage, Legal Tender, and the Reserve Bank of India. Additional Key Points • Energy Infrastructure Damage: Experts warn that even a short-lived war could have long-term effects as rebuilding destroyed energy hubs in West Asia may take years, keeping energy \'risk premiums\' high. • The 1973 Comparison: The current surge is being likened to the first \'Oil Shock,\' emphasizing that the impact on global trade and supply routes (like the Red Sea/Suez Canal) could be structural rather than transitory. • Fiscal-Monetary Coordination: Elevated fuel prices may prompt the government to reduce excise duties to cool inflation, which would impact fiscal deficit targets, creating a complex environment for the RBI\'s April policy. Conclusion The upcoming RBI policy decision is a litmus test for India\'s macro-economic resilience. While domestic fundamentals were strong entering 2026, the exogenous shock of the West Asia war has reintroduced the twin threats of high inflation and stunted growth. A rate pause combined with a \'hawkish\' or cautious tone appears the most likely path to preserve financial stability without choking off the post-pandemic growth momentum. UPSC Relevance • GS Paper III: Indian Economy and issues relating to planning, mobilization of resources, growth, development, and employment. Specifically, the role of the RBI, monetary policy tools, and the impact of global events on the domestic economy. • GS Paper II: Effect of policies and politics of developed and developing countries on India’s interests (Geopolitics of Oil).

Address : 506, 3rd EYE THREE (III), Opp. Induben Khakhrawala, Girish Cold Drink Cross Road, CG Road, Navrangpura, Ahmedabad, 380009.

Mobile : 8469231587 / 9586028957

Telephone : 079-40098991

E-mail: dics.upsc@gmail.com

Address: A-306, The Landmark, Urjanagar-1, Opp. Spicy Street, Kudasan – Por Road, Kudasan, Gandhinagar – 382421

Mobile : 9723832444 / 9723932444

E-mail: dics.gnagar@gmail.com

Address: 2nd Floor, 9 Shivali Society, L&T Circle, opp. Ratri Bazar, Karelibaugh, Vadodara, 390018

Mobile : 9725692037 / 9725692054

E-mail: dics.vadodara@gmail.com

Address: 403, Raj Victoria, Opp. Pal Walkway, Near Galaxy Circle, Pal, Surat-394510

Mobile : 8401031583 / 8401031587

E-mail: dics.surat@gmail.com

Address: 303,305 K 158 Complex Above Magson, Sindhubhavan Road Ahmedabad-380059

Mobile : 9974751177 / 8469231587

E-mail: dicssbr@gmail.com

Address: 57/17, 2nd Floor, Old Rajinder Nagar Market, Bada Bazaar Marg, Delhi-60

Mobile : 9104830862 / 9104830865

E-mail: dics.newdelhi@gmail.com