Ahmedabad

(Head Office)Address : 506, 3rd EYE THREE (III), Opp. Induben Khakhrawala, Girish Cold Drink Cross Road, CG Road, Navrangpura, Ahmedabad, 380009.

Mobile : 8469231587 / 9586028957

Telephone : 079-40098991

E-mail: dics.upsc@gmail.com

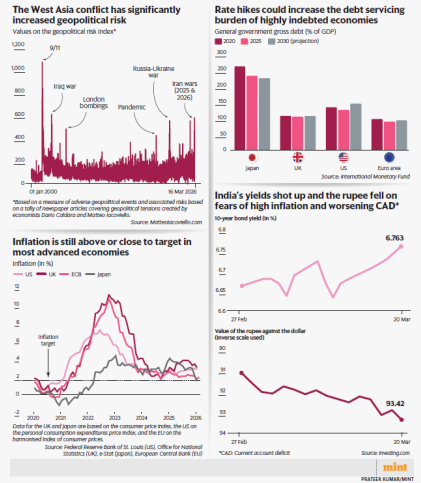

The recent escalation in West Asia, particularly the conflict involving the US, Israel, and Iran, has significantly disrupted the global economic recovery path. This crisis has forced major central banks to shift from planned rate cuts to a cautious \'wait-and-watch\' stance due to supply-side shocks and energy insecurity. Core Summary of the Global Economic Crisis • Policy Turnaround: Major central banks, including the US Fed, ECB, and Bank of England, have paused their interest rate trajectories. The closure of the Strait of Hormuz—a vital energy transit point—has invalidated earlier projections of rate cuts, forcing a shift to neutral stances. • Systemic Geopolitical Uncertainty: The world is transitioning from a US-led rules-based order to a multi-polar landscape. Persistent shocks from the pandemic, the Russia-Ukraine war, and now the West Asian conflict have created a cumulative stress level that tests the predictive capabilities of modern policymakers. • The Threat of Stagflation: With crude oil prices sustained above $100 per barrel, economies face Stagflation—a condition where inflation remains high while economic growth stagnates. This renders traditional monetary tools less effective, as hiking rates to curb inflation further hurts growth. • Energy Vulnerability: While the US is a major producer, regions like Japan and Europe are highly dependent on West Asian imports. High crude prices act as a \'tax on consumption,\' increasing costs for fertilizers, plastics, and transport, thereby spilling over into core inflation. • Fiscal and Debt Constraints: Sovereign debt-to-GDP ratios are at record highs (e.g., Japan at 227%, US at 129%). Tightening monetary policy to fight inflation increases the interest burden on government debt, potentially leading to a debt-sustainability crisis if growth does not outpace interest rates. • Impact on the Indian Economy: India faces a \'triple whammy\' of rising inflation, currency depreciation (Rupee at 93/$), and widening Current Account Deficit (CAD). The RBI’s room for rate cuts has vanished, as lowering rates could trigger capital flight and further weaken the Rupee. Key Concepts and Definitions • Stagflation: A simultaneous increase in inflation and stagnation of economic output, often accompanied by high unemployment. • Monetary Policy Transmission: The process through which central bank rate changes affect the overall price level and GDP of an economy. • Current Account Deficit (CAD): A measurement of a country\'s trade where the value of the goods and services it imports exceeds the value of the products it exports. • Overnight Indexed Swaps (OIS): A derivative contract where a fixed rate is swapped against a floating overnight reference rate; it serves as a market indicator for future interest rate expectations. Constitutional and Legal Context • RBI Act, 1934: Provides the legal framework for the Monetary Policy Committee (MPC) to maintain price stability while keeping in mind the objective of growth. • FRBM Act, 2003: The Fiscal Responsibility and Budget Management Act mandates the government to ensure inter-generational equity in fiscal management and long-term macro-economic stability. • Article 292: Empowers the Union Government to borrow upon the security of the Consolidated Fund of India within limits set by Parliament. Conclusion The convergence of war in West Asia and record-high global debt has created a policy \'freeze.\' For India, the resilience of the domestic economy will depend on the RBI’s ability to remain flexible and the government\'s capacity to manage fiscal slippages arising from higher energy subsidies and import bills. Navigating this multipolar, uncertain era requires a delicate balance between containing imported inflation and supporting domestic manufacturing. UPSC Relevance • GS Paper II: Effect of policies and politics of developed and developing countries on India\'s interests (Geopolitical impact of West Asian War). • GS Paper III: Indian Economy and issues relating to planning, mobilization of resources, growth, and development; Inflationary trends and Monetary Policy. • Prelims: Concepts like Stagflation, CAD, OIS, and the functions of the Monetary Policy Committee (MPC).

Address : 506, 3rd EYE THREE (III), Opp. Induben Khakhrawala, Girish Cold Drink Cross Road, CG Road, Navrangpura, Ahmedabad, 380009.

Mobile : 8469231587 / 9586028957

Telephone : 079-40098991

E-mail: dics.upsc@gmail.com

Address: A-306, The Landmark, Urjanagar-1, Opp. Spicy Street, Kudasan – Por Road, Kudasan, Gandhinagar – 382421

Mobile : 9723832444 / 9723932444

E-mail: dics.gnagar@gmail.com

Address: 2nd Floor, 9 Shivali Society, L&T Circle, opp. Ratri Bazar, Karelibaugh, Vadodara, 390018

Mobile : 9725692037 / 9725692054

E-mail: dics.vadodara@gmail.com

Address: 403, Raj Victoria, Opp. Pal Walkway, Near Galaxy Circle, Pal, Surat-394510

Mobile : 8401031583 / 8401031587

E-mail: dics.surat@gmail.com

Address: 303,305 K 158 Complex Above Magson, Sindhubhavan Road Ahmedabad-380059

Mobile : 9974751177 / 8469231587

E-mail: dicssbr@gmail.com

Address: 57/17, 2nd Floor, Old Rajinder Nagar Market, Bada Bazaar Marg, Delhi-60

Mobile : 9104830862 / 9104830865

E-mail: dics.newdelhi@gmail.com