Ahmedabad

(Head Office)Address : 506, 3rd EYE THREE (III), Opp. Induben Khakhrawala, Girish Cold Drink Cross Road, CG Road, Navrangpura, Ahmedabad, 380009.

Mobile : 8469231587 / 9586028957

E-mail: dics.upsc@gmail.com

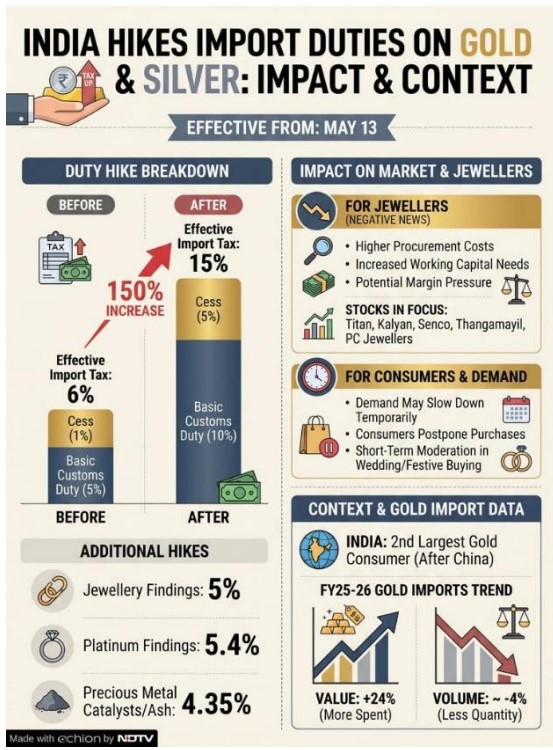

• Significant Duty Revision: The Union Government has doubled the effective tax on gold and silver imports from 9.2% to 18.4% to curb non-essential outflows and stabilize the external sector.

• Fiscal Mechanism: This change involves raising the Basic Customs Duty (BCD) to 10% and the Agriculture Infrastructure and Development Cess (AIDC) to 5%, calculated alongside the existing 3% IGST on the total assessable value.

• Strategic Rationalization: The decision is primarily driven by the West Asia crisis and global volatility in crude oil markets, which threaten to expand India\'s Current Account Deficit (CAD) and deplete foreign exchange reserves.

• Prioritizing Essentials: By making precious metals more expensive, the government aims to redirect foreign exchange towards essential imports like fertilizers, crude oil, defense equipment, and critical technologies.

• Monetary & Currency Stability: The hike aligns with efforts to protect the Indian Rupee exchange rate against a strengthening dollar and ensures prudent management of the country Balance of Payments (BoP).

• Sectoral Concerns: Industry experts warn that the move might be retrograde, potentially incentivizing smuggling and gray market transactions due to the inelastic cultural demand for gold in India.

Key Definitions

• Current Account Deficit (CAD): A measurement of a country trade where the value of the goods and services it imports exceeds the value of the products it exports.

• Agriculture Infrastructure and Development Cess (AIDC): A tax levied by the government to raise funds for improving agriculture infrastructure, applied over and above the basic customs duty.

• Assessable Value: The total value determined by customs authorities (Cost + Insurance + Freight) upon which duties and taxes are calculated.

Constitutional and Legal Provisions

• Article 265: No tax shall be levied or collected except by authority of law; the duty hike is implemented via notifications under the Customs Act, 1962.

• Article 269A: Relates to the levy and collection of IGST on supplies in the course of inter-state trade or commerce, including imports.

• Customs Act, 1962: Provides the legal framework for the levy of duties on imports and exports and the regulation of the same to prevent smuggling.

Economic Context & Impact Analysis

• BoP Management: Gold is often the second-largest item in India import bill after crude oil. Reducing its volume is a standard tool for managing the Balance of Payments (BoP).

• Inflationary Pressure: While the duty aims to save forex, it may lead to higher domestic prices for jewelry, potentially impacting the gems and jewelry sector\'s contribution to GDP and employment.

• The Smuggling Paradox: High duty differentials between domestic and international prices historically lead to an increase in illicit trade, which poses a challenge for enforcement agencies like the Directorate of Revenue Intelligence (DRI).

Conclusion The doubling of import duties on gold and silver reflects a stability-first approach by the government amidst global geopolitical turbulence. While it serves as a necessary fiscal buffer to protect the CAD and foreign exchange reserves, its success depends on balancing domestic demand with the need for external sector resilience without inadvertently fueling the shadow economy.

UPSC Relevance

• General Studies III (Economy): Issues relating to mobilization of resources, government budgeting, and effects of liberalization on the economy.

• General Studies II: Statutory, regulatory, and various quasi-judicial bodies (Role of Ministry of Finance and CBIC).

• Prelims: Concepts like CAD, BoP, AIDC, and the impact of customs duty on currency exchange rates.

Address : 506, 3rd EYE THREE (III), Opp. Induben Khakhrawala, Girish Cold Drink Cross Road, CG Road, Navrangpura, Ahmedabad, 380009.

Mobile : 8469231587 / 9586028957

E-mail: dics.upsc@gmail.com

Address: A-306, The Landmark, Urjanagar-1, Opp. Spicy Street, Kudasan – Por Road, Kudasan, Gandhinagar – 382421

Mobile : 9723832444 / 9723932444

E-mail: dics.gnagar@gmail.com

Address: 2nd Floor, 9 Shivali Society, L&T Circle, opp. Ratri Bazar, Karelibaugh, Vadodara, 390018

Mobile : 9725692037 / 9725692054

E-mail: dics.vadodara@gmail.com

Address: 403, Raj Victoria, Opp. Pal Walkway, Near Galaxy Circle, Pal, Surat-394510

Mobile : 8401031583 / 8401031587

E-mail: dics.surat@gmail.com

Address: 303,305 K 158 Complex Above Magson, Sindhubhavan Road Ahmedabad-380059

Mobile : 9974751177 / 8469231587

E-mail: dicssbr@gmail.com

Address: 57/17, 2nd Floor, Old Rajinder Nagar Market, Bada Bazaar Marg, Delhi-60

Mobile : 9104830862 / 9104830865

E-mail: dics.newdelhi@gmail.com