Ahmedabad

(Head Office)Address : 506, 3rd EYE THREE (III), Opp. Induben Khakhrawala, Girish Cold Drink Cross Road, CG Road, Navrangpura, Ahmedabad, 380009.

Mobile : 8469231587 / 9586028957

E-mail: dics.upsc@gmail.com

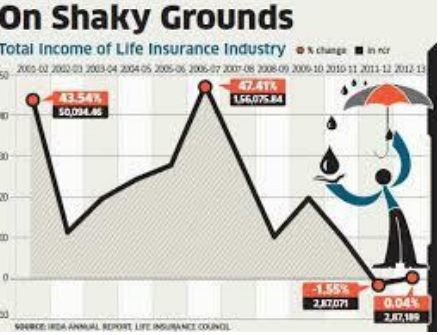

The Indian life insurance industry is witnessing a structural faultline characterized by a sharp divergence between premium growth and distribution costs. While the industry paid ₹60,799 crore in commissions in FY2025, the alarming trend lies in the 18% surge in payouts against a modest 6.7% growth in premiums. This escalation, flagged by the RBI in its Financial Stability Report, suggests that bargaining power has shifted heavily toward corporate intermediaries, potentially eroding value for policyholders. Structural Faultlines and Key Highlights • Rising Acquisition Costs: Distribution costs are currently rising nearly three times faster than the business they support, indicating a significant drop in operational efficiency across the sector. • Public-Private Divergence: LIC, with its agency-dominated model, reduced its commission ratio to 5.17%, whereas private insurers reliant on alternate channels (banks/brokers) saw ratios jump to 8.95%. • Concentrated Bargaining Power: The \'Bancassurance\' model has created an imbalance where banks, controlling over 4,00,000 branches, dictate terms to insurers, leading to commission inflation rather than competitive pricing for consumers. • The EOM Framework Paradox: The shift to the Expenses of Management (EOM) framework in 2023-24 aimed at transparency, but instead allowed institutional intermediaries to assertively demand higher payouts previously hidden in other accounting heads. • Impact on Penetration: Insurance penetration has declined from 4% to 3.7% of GDP. Rising acquisition costs risk making insurance products unviable for middle-income households, threatening the \'Insurance for All by 2047\' vision. • Incentive Misalignment: Current distribution economics favor \'front-loading\' (high initial commissions) over \'renewal income,\' which prioritizes immediate sales over long-term policy persistency and service quality. Constitutional & Legal Provisions • Article 38 (DPSP): Mandates the State to promote the welfare of the people by securing a social order in which justice—social, economic, and political—informs all institutions, including fair financial services. • Insurance Act, 1938: The primary legislation governing the sector. Section 402A (inserted later) deals with the limitation of expenses of management in life insurance business.• IRDAI Act, 1999: Established the Insurance Regulatory and Development Authority of India (IRDAI) to protect the interests of policyholders and regulate the orderly growth of the industry. • IRDAI (Expenses of Management) Regulations, 2023: Replaced specific commission caps with an aggregate EOM limit, providing insurers more flexibility but requiring stricter board-level oversight. Definitions of Key Terms • Bancassurance: A partnership between a bank and an insurance company that allows the insurance company to sell its products to the bank\'s client base. • Commission Ratio: The percentage of premium income that is paid out as commission to intermediaries; a rising ratio indicates higher costs of acquiring new business. • Persistency Ratio: The percentage of policies remaining in force over a specific period; it is a key metric for measuring customer satisfaction and long-term value. • Front-loading: A commission structure where a disproportionately high percentage of the total commission is paid in the first year of the policy. • Open Architecture: A regulatory setup where a single distributor (like a bank) can sell products from multiple insurance companies to promote competition. Conclusion The escalation of distribution costs is not a mere compliance failure but a structural market issue. To safeguard the industry\'s sustainability, the regulatory focus must shift from process-based compliance to outcome-based metrics like service satisfaction and claims experience. Rebalancing incentives toward renewal income and establishing joint RBI-IRDAI oversight for Bancassurance are essential steps to ensure that the bargaining power of distributors does not come at the cost of the common policyholder\'s savings. UPSC Relevance • Prelims: Understanding IRDAI and RBI mandates; basic concepts like Bancassurance, EOM, and Insurance Penetration vs. Density. • Mains (GS Paper III): Mobilization of Resources; Indian Economy and issues relating to planning and growth; Impact of financial sector regulations on inclusive growth and social security

Address : 506, 3rd EYE THREE (III), Opp. Induben Khakhrawala, Girish Cold Drink Cross Road, CG Road, Navrangpura, Ahmedabad, 380009.

Mobile : 8469231587 / 9586028957

E-mail: dics.upsc@gmail.com

Address: A-306, The Landmark, Urjanagar-1, Opp. Spicy Street, Kudasan – Por Road, Kudasan, Gandhinagar – 382421

Mobile : 9723832444 / 9723932444

E-mail: dics.gnagar@gmail.com

Address: 2nd Floor, 9 Shivali Society, L&T Circle, opp. Ratri Bazar, Karelibaugh, Vadodara, 390018

Mobile : 9725692037 / 9725692054

E-mail: dics.vadodara@gmail.com

Address: 403, Raj Victoria, Opp. Pal Walkway, Near Galaxy Circle, Pal, Surat-394510

Mobile : 8401031583 / 8401031587

E-mail: dics.surat@gmail.com

Address: 303,305 K 158 Complex Above Magson, Sindhubhavan Road Ahmedabad-380059

Mobile : 9974751177 / 8469231587

E-mail: dicssbr@gmail.com

Address: 57/17, 2nd Floor, Old Rajinder Nagar Market, Bada Bazaar Marg, Delhi-60

Mobile : 9104830862 / 9104830865

E-mail: dics.newdelhi@gmail.com