Ahmedabad

(Head Office)Address : 506, 3rd EYE THREE (III), Opp. Induben Khakhrawala, Girish Cold Drink Cross Road, CG Road, Navrangpura, Ahmedabad, 380009.

Mobile : 8469231587 / 9586028957

E-mail: dics.upsc@gmail.com

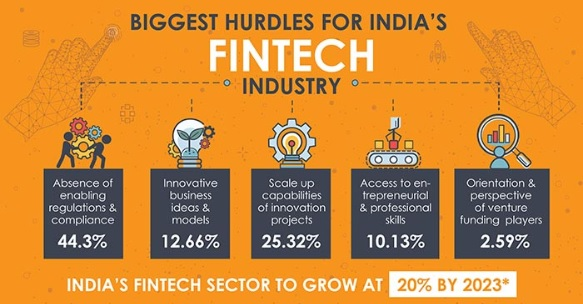

Fintech sector in India

News: The Parliamentary Standing Committee on Communications and Information Technology presented a report to the Parliament on February 8, 2024, raising concerns about the dominance of fintech apps owned by foreign entities in the Indian ecosystem.

Key Findings:

• The Committee recommended promoting local players as they observed that fintech companies, apps, and platforms owned by foreign entities, such as Walmart-backed PhonePe and Google Pay, dominate the Indian fintech sector.

• The Unified Payments Interface (UPI) commanded a 73.5% share of the total digital payments in terms of volume in FY 2022-23. However, its share in terms of value was only 6.67% in the same period.

• Scammers have been using these financial companies to dupe people and launder illegitimate money. For instance, Abu Dhabi-based app called Pyppl, operated by the Chinese investment scammers was used for money laundering in India.

Key recommendations:

• The Committee emphasized that digital payment apps must be effectively regulated as the use of digital platforms to make payments in India is on the rise.

• It will be more ‘feasible’ for regulatory bodies such as the Reserve Bank of India (RBI) and the National Payments Corporation of India (NPCI) to control local apps, as compared with foreign apps, which operate in multiple jurisdictions.

• The NPCI’s BHIM UPI’s market share (in terms of volume) stood at a mere 0.22%.

• The NPCI issued a 30% volume cap on transactions facilitated using UPI, back in November 2020. The timeline for compliance was extended in December 2022 to December 31, 2024.

What is Fintech?

• Fintech, a portmanteau of “financial technology”, refers to the integration of technology into offerings by financial services companies to improve their use and delivery to consumers. It primarily works by unbundling offerings by such firms and creating new markets for them.

• Fintech covers various sectors and industries, such as banking, insurance, investment, and crypto.

Fintech adoption in India:

• With a fintech adoption rate at 87% against the global average of 64%, India has emerged as one of the largest digital markets in the world.

• India is the 3rd largest FinTech ecosystem. 17 Indian Fintech companies have gained ‘Unicorn Status’ as on Dec 2021.

• The Indian Govt initiatives such as the JAM trinity, India Stack, Open Network for Digital Commerce (ONDC), Unified Payments Interface (UPI), and Central Bank Digital Currency (CBDC), have the growth of Fintechs in India.

What are the benefits of the Fintech Sector?

• Increased Efficiency: Fintech applications help companies, business owners, and consumers better manage their financial operations, processes, and lives. They streamline financial transactions and investment processes, improving organizations’ proficiency and growth.

• Lower Costs: Fintech companies use technology to cut down on operational costs. Adopting new financial

technologies does not require radical infrastructure transformation or significant investment.

• Promotion of Financial Inclusion: Innovation driven by Fintech has widened citizen’s access to financial services.

• Improved Credit availability: Lending Fintechs have improved credit availability options for the financially marginalised sections in India.

• Improved Financial Habits: Fintech applications can help users track their finances, giving them greater control and promoting improved financial habits.

• Improved Customer Experience: Fintechs have improved the customer service experience in financial sector by employing leveraging big data, machine learning tools. For instance, ease of investment in share markets by Zerodha.

What are the concerns with Fintech sector in India?

• Data and Payment Security: As financial transactions increasingly move online, ensuring the security of data and payments is a significant challenge.

• Compliance: Fintech companies must comply with various regulations set by bodies like the Reserve Bank of India (RBI), Securities and Exchange Board of India (SEBI), etc. This can be complex and costly.

• Lack of Awareness: Many end-users lack awareness about fintech services, which can hinder adoption.

• Working Alongside Legacy Systems: Integrating fintech solutions with existing banking and financial systems can be challenging.

• Cybersecurity concerns: The Fintech startups are vulnerable to cyber-attacks and hacking. According to the CERT-In data, a total of 13.91 lakh cases of cyber-attacks were reported in India.

How is the Indian government regulating fintech companies?

• Payment and Settlement Systems Act, 2007: It forbids the establishment and operation of any ‘payment system’ in India without the prior approval of the RBI.

• RBI Guidelines on Digital Lending 2022: It aims to bring unregulated digital lending players within the RBI’s ambit and create a comprehensive framework to protect consumers’ data.

• RBI Regulatory Sandbox Framework 2019: It allows FinTech companies to test their products and services in a controlled environment. It helps in fostering innovation while maintaining regulatory oversight.

Address : 506, 3rd EYE THREE (III), Opp. Induben Khakhrawala, Girish Cold Drink Cross Road, CG Road, Navrangpura, Ahmedabad, 380009.

Mobile : 8469231587 / 9586028957

E-mail: dics.upsc@gmail.com

Address: A-306, The Landmark, Urjanagar-1, Opp. Spicy Street, Kudasan – Por Road, Kudasan, Gandhinagar – 382421

Mobile : 9723832444 / 9723932444

E-mail: dics.gnagar@gmail.com

Address: 2nd Floor, 9 Shivali Society, L&T Circle, opp. Ratri Bazar, Karelibaugh, Vadodara, 390018

Mobile : 9725692037 / 9725692054

E-mail: dics.vadodara@gmail.com

Address: 403, Raj Victoria, Opp. Pal Walkway, Near Galaxy Circle, Pal, Surat-394510

Mobile : 8401031583 / 8401031587

E-mail: dics.surat@gmail.com

Address: 303,305 K 158 Complex Above Magson, Sindhubhavan Road Ahmedabad-380059

Mobile : 9974751177 / 8469231587

E-mail: dicssbr@gmail.com

Address: 57/17, 2nd Floor, Old Rajinder Nagar Market, Bada Bazaar Marg, Delhi-60

Mobile : 9104830862 / 9104830865

E-mail: dics.newdelhi@gmail.com