Ahmedabad

(Head Office)Address : 506, 3rd EYE THREE (III), Opp. Induben Khakhrawala, Girish Cold Drink Cross Road, CG Road, Navrangpura, Ahmedabad, 380009.

Mobile : 8469231587 / 9586028957

E-mail: dics.upsc@gmail.com

Co-operative societies are not Banks

News: The Reserve Bank of India (RBI) has cautioned members of the public not to deal with cooperative societies undertaking banking business by adding ‘bank’ to their names.

Details:

• It has also come to the notice of RBI that some co-operative societies are accepting deposits from nonmembers/nominal members/ associate members.This is tantamount to conducting banking business in violation of the provisions.

• The Banking Regulation Act, 1949 was amended by the Banking Regulation (Amendment) Act, 2020, which came into force on September 29, 2020.Accordingly, co-operative societies cannot use the words “bank”, “banker” or “banking” as part of their names, except as permitted under the provisions of BR Act, 1949 or by the RBI.

What is Cooperative Banking?

• Cooperatives are people-centred enterprises owned, controlled and run by and for their members to realise their common economic, social, and cultural needs and aspirations.Cooperative bank is an institution established on the cooperative basis and dealing in ordinary banking business.Like other banks, the cooperative banks are founded by collecting funds through shares, accept deposits and grant loans.

• They are regulated by the Reserve Bank of India (RBI) and governed by the

• Banking Regulations Act 1949

• Banking Laws (Co-operative Societies) Act, 1955

• Cooperative banks are generally concerned with the rural credit and provide financial assistance for agricultural and rural activities.Such banking in India is federal in structure. Primary credit societies are at the lowest rung.

• Then, there are central cooperative banks at the district level and state cooperative banks at the state level.

• Cooperative credit societies are mostly located in villages spread over the entire country.

• The cooperative movement in India was started primarily for dealing with the problem of rural credit.

• The history of Indian cooperative banking started with the passing of Cooperative Societies Act in 1904.

• The objective of this Act was to establish cooperative credit societies “to encourage thrift, self-help and cooperation among agriculturists, artisans and persons of limited means.”

• Many cooperative credit societies were set up under this Act.The Cooperative Societies Act, 1912 recognised the need for establishing new organisations for supervision, auditing and supply of cooperative credit.

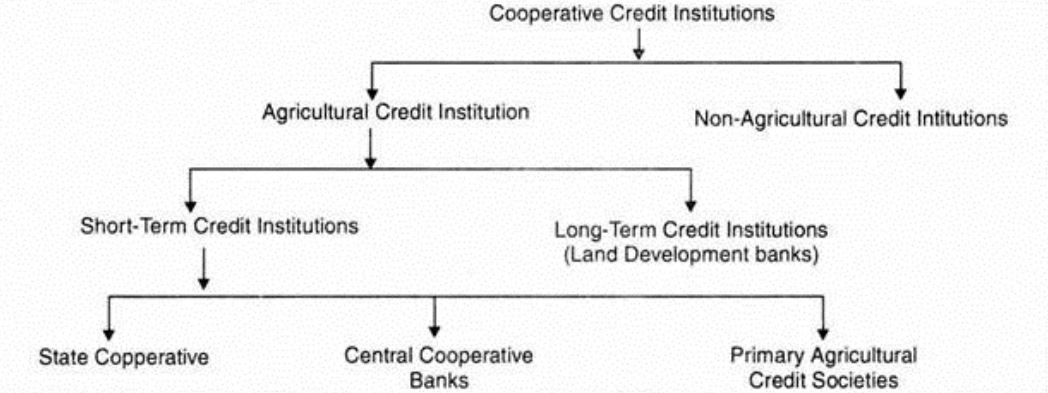

• The whole structure of cooperative credit institutions is shown in the chart given.

• There are different types of cooperative credit institutions working in India.

• These institutions can be classified into two broad categories- agricultural and non-agricultural.

• Agricultural credit institutions dominate the entire cooperative credit structure.

• Cooperatives in India have grown exponentially.In the banking sector, according to the RBI, their contribution to rural credit increased from 3.1 percent in 1951 to an impressive 27.3 percent in 2002.

Importance of Cooperative Banks:

• The cooperative banking system has to play a critical role in promoting rural finance and is especially suited to Indian conditions.The main objective of the cooperative credit movement is to provide an effective alternative to the traditional defective credit system of the village moneylender.

• Cooperative credit system has cheapened the rural credit by charging comparatively low-interest rates, and has broken the money lender’s monopoly.

• The cultivators used to borrow for consumption and other unproductive purposes. But, now, they mostly borrow for productive purposes.Instead of hoarding money the rural people tend to deposit their savings in cooperative or other banking institutions.

• Cooperative credit is available for purchasing improved seeds, chemical fertilizers, modern implements, etc.

• They have played a significant role in the financial inclusion of unbanked rural masses. They provide cheap credit to the masses in rural areas.

Address : 506, 3rd EYE THREE (III), Opp. Induben Khakhrawala, Girish Cold Drink Cross Road, CG Road, Navrangpura, Ahmedabad, 380009.

Mobile : 8469231587 / 9586028957

E-mail: dics.upsc@gmail.com

Address: A-306, The Landmark, Urjanagar-1, Opp. Spicy Street, Kudasan – Por Road, Kudasan, Gandhinagar – 382421

Mobile : 9723832444 / 9723932444

E-mail: dics.gnagar@gmail.com

Address: 2nd Floor, 9 Shivali Society, L&T Circle, opp. Ratri Bazar, Karelibaugh, Vadodara, 390018

Mobile : 9725692037 / 9725692054

E-mail: dics.vadodara@gmail.com

Address: 403, Raj Victoria, Opp. Pal Walkway, Near Galaxy Circle, Pal, Surat-394510

Mobile : 8401031583 / 8401031587

E-mail: dics.surat@gmail.com

Address: 303,305 K 158 Complex Above Magson, Sindhubhavan Road Ahmedabad-380059

Mobile : 9974751177 / 8469231587

E-mail: dicssbr@gmail.com

Address: 57/17, 2nd Floor, Old Rajinder Nagar Market, Bada Bazaar Marg, Delhi-60

Mobile : 9104830862 / 9104830865

E-mail: dics.newdelhi@gmail.com